HMRC created the research and development tax relief scheme to stimulate scientific and technical innovation. The Treasury made its R&D claim PAYE cap public in late 2020. This relief is offered to corporations and considerably reduces their tax bills. Chancellor Rishi Sunak confirmed in his 2021 Budget address that the cap will take effect on the first accounting period commencing on or after April 1, 2021. This implies that if your business files its financial statements on December 31, the first accounting period for which the cap would be imposed will be the fiscal year ending December 31, 2022.

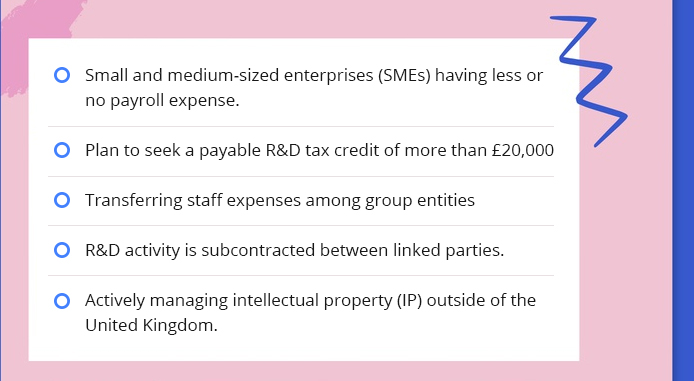

However, SME R&D tax credit claims have started from April 1, 2021, subjected to a cap. This cap may limit the amount of cash value accessible to firms and will largely affect those in the UK without significant payroll expenses. Policymakers are increasingly concerned about whether the R&D tax credit incentive is being abused. The issue is discovered on the annual survey of business enterprise research and development (BERD). As an anti-abuse measure, the cap restricts the cash benefit that businesses may get under the R&D Tax Credits scheme to

- £20,000 plus

- 300 percent of their PAYE and NIC (National Insurance Contributions) liabilities for the claiming period.

The National Audit Office classified low-quality and fraudulent R&D claims as the “main cause of lost tax” in the UK in early 2020.

Will I be affected by the PAYE/NIC cap?

To reduce the impact on legitimate enterprises, the cap now incorporates the following features:

- The cap will not apply to a firm that makes a modest claim for payment credit of less than £20,000.

- A company's claim, regardless of size, will be uncapped if two conditions are met. These tests demand that:

- Its employees are developing, planning to develop, or actively managing intellectual property (Here IP covers any trademark, patent, copyright, registered design, design right, performer’s right, or plant breeder’s right for these purposes).

- And its expenses on work subcontracted to or externally provided workers furnished by, associated party accounts for less than 15% of its total R&D expenditure.

R&D costs are exorbitantly expensive, high-risk endeavors; thus it is uncommon for smaller, R&D-intensive firms to incur tax losses and/or rely on outside resources before they are ready to hire staff. The cash credit component of SME R&D tax relief is specifically designed to provide a critical financial infusion in these instances. However, the cap may cause that funding to be delayed for years.

In case of your R&D tax credit is capped, you will receive less money. The remaining amount will be carried forward as a trading loss and may be deducted against future taxable earnings. Many businesses that do R&D initiatives each year will include the tax credit financing into their annual cash flow.

Why the new PAYE and NIC cap?

HMRC publishes yearly statistics on R&D tax credit claims, which have recently included a comparison of BERD spending declared and R&D expenditure on which a claim for R&D tax credits has been lodged. According to this comparison, there is a significant gap between the volume of R&D being conducted in the United Kingdom and the actual monetary amounts being paid out under the R&D tax credit incentive. We are not talking about hundreds of pounds here: we are talking billions! According to the statistics, almost £10 billion in R&D investment has gone missing.

Case Study/Illustration

A recent scam of £29.5 million in R&D tax relief provided a compelling illustration of how the benefit is being misused. Three men were sentenced to a total of 21 years in prison for their involvement in a fraudulent £29.5 million claim for a research and development (R&D) tax rebate on a fake IT project. According to Birmingham Crown Court, Matthew Sutherland was the mastermind of the crime, claiming tax relief of £29.5 million against a purported £137 million spend on developing an IT healthcare system for two Middle Eastern countries through his company, Convergica (Clinical Information Systems) Ltd. In January 2016, a forged bank statement was filed, sparking an inquiry that resulted in the arrests of Sutherland and the other guy. In March 2018, all three were prosecuted for fraud, and the claim was not paid out by HMRC.

HMRC appears to be more concerned that some black sheep are actively attempting to exploit the relief by constructing fake entities to obtain large cash payments. We applaud their initiative to minimise the amount of false and low-quality claims. This can only lead to the initiative achieving its stated goal of strengthening the UK economy via innovation. When it comes to R&D claims, now is not the time to keep doing what has worked in the past. We recommend you take the advantage of the chance to assess your claim and check that you are maximising its worth minimising its risks.